You have probably seen the phrase "real world assets" thrown around since 2023, often attached to a chart showing exponential growth. The concept sounds straightforward: take a treasury bond, a rental property, or a bar of gold and put it on a blockchain. But that framing is precisely where most people's understanding starts to fracture. RWA tokenisation is not the act of placing a physical or financial asset on a blockchain. It is the legal and technical process of representing rights to an off-chain asset as an on-chain token. The asset itself — the bond sitting in a custodian's account, the property deed registered with a county recorder — never moves onto Ethereum or any other chain. What moves on-chain is a digital claim, and the value of that claim depends entirely on the enforceability of the legal agreements underpinning it.

The taxonomy of tokenisable assets is broader than most people realise. Financial instruments include government treasuries, corporate bonds, equities, and fund units. Real assets cover real estate, commodities like gold and oil, and agricultural products. Intangible assets span intellectual property, carbon credits, revenue streams, and even trade receivables. Each category carries different legal, custodial, and regulatory requirements, which is why tokenised US Treasuries have scaled to ~$6.5 billion while tokenised real estate remains comparatively niche. The convergence of higher interest rates (making treasury yield worth tokenising), maturing blockchain infrastructure, post-ETF institutional comfort, and regulatory sandboxes opening in the UK, EU, Singapore, and Hong Kong has created the conditions for the market to cross ~$20.5 billion in on-chain value (excluding stablecoins) as of Q1 2026 — up from roughly $1.5 billion in 2022.

One terminology distinction matters more than most guides acknowledge. The crypto industry uses "RWA" broadly. Regulators use "digital securities" or "tokenised financial instruments" — and the difference is not semantic. Calling something an RWA has no legal meaning. Calling it a digital security triggers specific registration, disclosure, and custody obligations. When you evaluate any RWA project, the first question is not "what chain is it on?" but "what does this token represent in a court of law?"

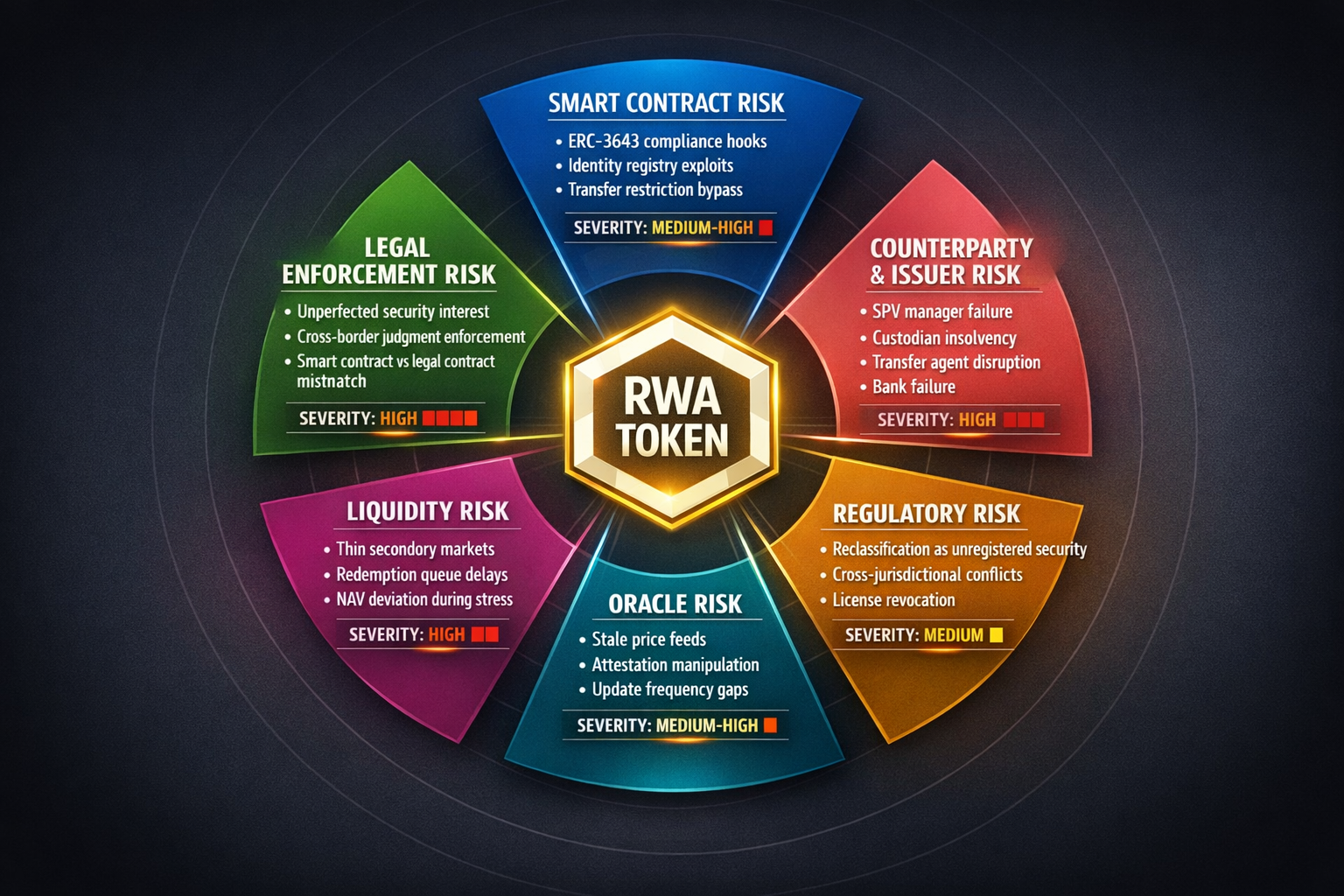

⚠ Common mistake: Treating all RWA tokens as interchangeable. A tokenised US Treasury held through a registered fund (BlackRock BUIDL) and a tokenised revenue share from an unregulated platform have radically different risk profiles despite both being labelled "RWA."